Most people don’t realize that modern logistics is no longer just physical—it’s increasingly digital. A digital twin...

-

-

-

-

Pickup

-

-

-

Minivan

-

-

-

2.5 T Closed cab truck

-

-

-

2,5T Flatbed truck

-

-

-

-

-

3T Flatbed Truck

-

3T closed Cab Truck

-

séparateur

-

-

-

5T Flatbed Truck

-

5T closed Cab Truck

-

-

-

10T Flatbed Truck

-

10T closed Cab Truck

-

-

-

-

-

Semi trailer truck

-

-

-

Semi remorque

-

-

-

Semi-tank truck

-

-

-

Semi Tipper Truck

-

-

-

-

-

-

Image & HTML

-

Refrigerated transportRefrigerated transport of food or pharmaceutical products such as vaccines from -20 ° C

-

Pallet transportPallet transport on demand or by grouping at an affordable price..

-

-

-

Image & HTML

-

Fleet management system TMSDigital fleet management solution, internal management of vehicles, drivers, expenses and income in Cloud mode with all web and mobile functionalities.

-

-

-

-

-

-

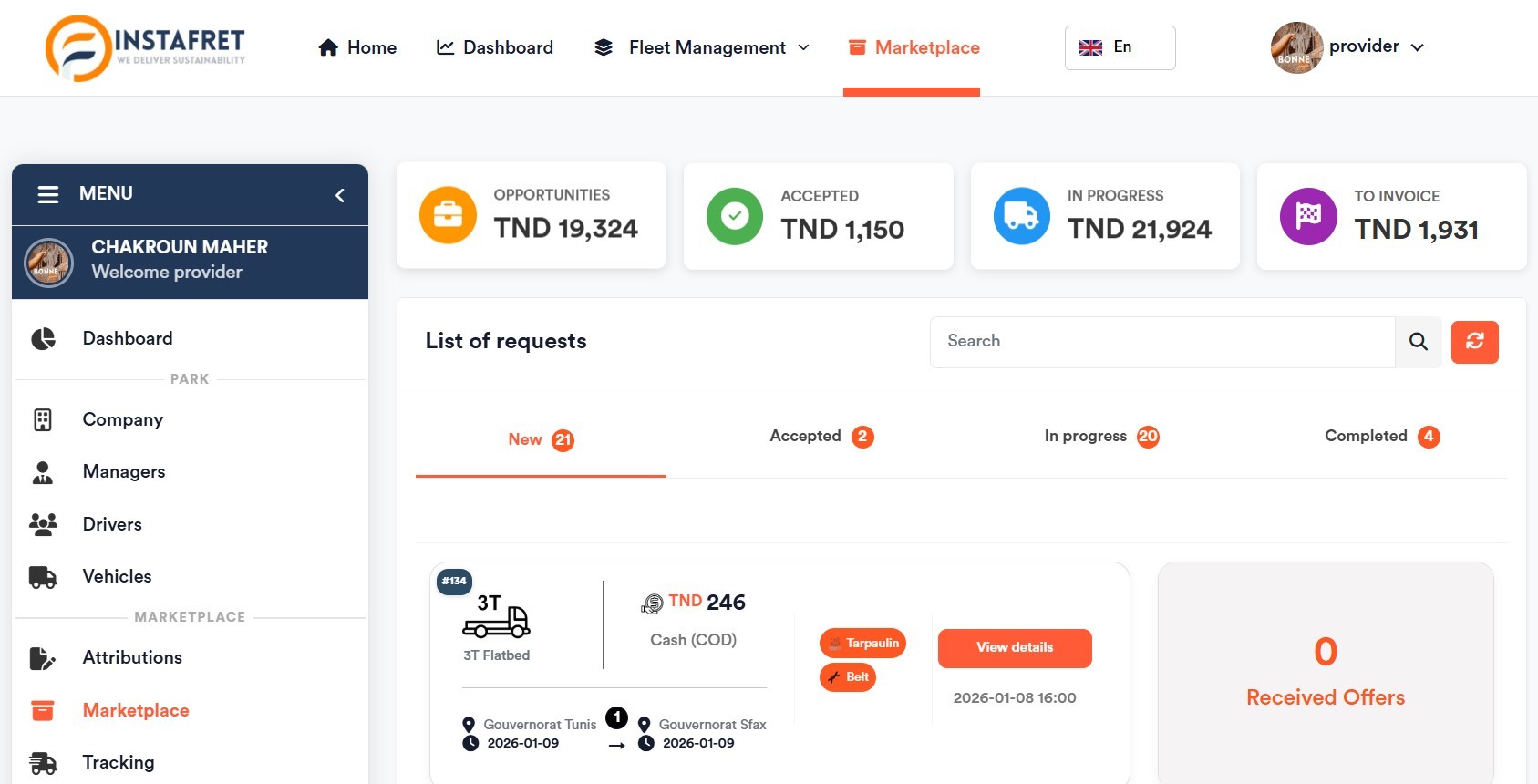

Marketplace LogistiqueSubscribe to our logistics Marketplace, centralize and optimize your business:

- Truck rental

- Handling services

- Warehousing services

- International transport

- Maritime transport

- Fleet management

-

INSTAFRET

-

-

-

Marketplace LogistiqueThanks to our ERP Entreprise Ressources Planning (Optifret), manage your real time business:

- E-invoice

- Invoicing

- HR Management

- Product/Services/stock management

- Sales management

- Fleet management

-

optifret Gestion complète

-

-

-

B2B E-COMMERCEThanks to our B2B E-Commerce Marketplace, manage your business in real time with the included logistics solution

- Online store

- Order management

- Online payment

- QR code Menu

- Commercial management

- Delivery management

-

DIGIMOLL B2B E-COMMERCE

-

-

Latest posts

-

Digital Twins are Transforming Supply ChainsRead more

Digital Twins are Transforming Supply ChainsRead more -

Optimalogistic annonce un partenariat stratégique avec CSPD SfaxRead more

Optimalogistic annonce un partenariat stratégique avec CSPD SfaxRead moreOptimalogistic est fier d’annoncer un nouveau partenariat stratégique avec CSPD Comptoir Sfaxien des Pneus Dammak,...

-

Optimalogistic at the Heart of Innovation & SafetyRead more

Optimalogistic at the Heart of Innovation & SafetyRead moreWe were honored to participate as an exhibitor and official transport provider for the Tunisian delegation at the...

-

Mission Affaire Dakar SénégalRead more

Mission Affaire Dakar SénégalRead moreOptimalogistic a participé en mois de Février dans une mission d'affaire au Sénégal

-

New law on bank check in TunisiaRead more

New law on bank check in TunisiaRead moreThis is an innovative law that aims to streamline the use of cheques, a payment instrument that is falling into...

-

Our COO selected within the TOP 100 Women entrepreneursRead more

Our COO selected within the TOP 100 Women entrepreneursRead moreWe are incredibly proud to announce that our COO and cofounder, Souhir Boujelbene, has been recognized as one of the...

-

Djerba Slush DRead more

Djerba Slush DRead moreSlush’D operates as an international entrepreneurship platform, linking startups, investors, corporate leaders, and...

-

Optimalogistic's Vision: Expanding the New Silk Road into AfricaRead more

Optimalogistic's Vision: Expanding the New Silk Road into AfricaRead moreThe Belt and Road Initiative, launched by China, aims to revitalize global trade and investment by connecting Asia to...

-

Optimalogistic selected as CCIS facilitator for the Techlog projectRead more

Optimalogistic selected as CCIS facilitator for the Techlog projectRead moreOptimalogistic was selected as an Innovation Facilitator for the CCIS as part of the TECHLOG project in order to...

-

Optimalogistic seleted as the Best scaling African Startup by SCIPRead more

Optimalogistic seleted as the Best scaling African Startup by SCIPRead moreOptimalogistic seleted as the Best scaling African Startup in 2022 by SCIP.

Blog categories

Search in blog

New law on bank check in Tunisia

Tunisia -Law no. 41-2024, which was promulgated on August 2, 2024 and mainly concerns the new regulation of cheques and will enter into force on February 2, is part of a series of groundbreaking reforms.

These reforms generally involve short-term costs, but generate significant future returns if properly implemented, banking and finance expert Ahmed El Karm told TAP.

This is an innovative law that aims to streamline the use of cheques, a payment instrument that is falling into disuse in most advanced economies and even in some developing countries where modern alternative payment instruments have been introduced.

Tunisia would do well to take inspiration from these models so that the reduction in the use of cheques is accompanied by the promotion of cheaper, safer and more practical means of payment, recommended El Karm, who is also Honorary President of the Tunisian Association for the Promotion of Financial Culture (ATCF).

Need to develop alternative payment instruments

He pointed out that there are many alternative means of payment. The first is payment cards, which are becoming increasingly popular in Tunisia. However, they are still dominated by cash withdrawals. Barely 40% of cards are used for commercial transactions.

(This may be due to the fact that payment by card requires traceability, which may discourage some merchants from using it), he adds. There is therefore a need to consider fiscal measures that would reduce the taxes levied on card transactions compared to those levied on bank notes.

Consideration should also be given to adjusting the system of bank charges by penalising cash withdrawals at bank counters and making it more advantageous to pay by card or other electronic means.

A whole series of accompanying measures must therefore be taken to encourage the development of card payments in Tunisia. Among payment instruments, El Karm also mentioned mobile payments, which have become commonplace for hundreds of millions of people in India, China and other Asian countries.

They are also commonplace in many other countries, particularly in sub-Saharan Africa, unlike Tunisia where this type of payment has not taken off as quickly as hoped.

Here too, El Karm believes that the government needs to work with banks, telephone operators and recently authorised payment institutions to make this form of payment as attractive as cash payments.

El Karm also spoke about e-commerce, which is still in its infancy in Tunisia, despite its growing share of the global market. With its young people, who are very familiar with modern technology, Tunisia has a great advantage in developing e-commerce and increasing the share of digital payments.

The rules governing this type of transaction need to be modernise, particularly to establish a solid relationship of trust between consumers and merchants and to move away from the practice of “cash and delivery.

Bank transfers are also among the instruments mentioned by our interviewee, who lamented the slowness of this means of payment in Tunisia. Bank transfers are one of the fastest means of payment in the world, thanks to completely secure computer software.

Transfers are available around the clock and take no more than 7 seconds. In Tunisia, bank transfers still take time to be credited to customers accounts, which puts them at a disadvantage compared to banknotes and cheques.

Again, there is room for improvement, especially as international standards have been adopted and implemented in several European partner countries.

No more backdated cheques

The new law also prohibits staggered payments through backdated cheques, which are widely used by consumers to pay for purchases in several instalments and by many small and medium-sized enterprises (SMEs) to pay their suppliers and manage their cash flow, although they were illegal under the old legislation.

The banking expert agrees that the ban on backdated cheques will have an impact on consumer habits and the cash management methods of SMEs, and believes that the implementation of this ban must be accompanied by measures to help individuals and businesses adapt to the new situation.

On the corporate side, he believes that banks are in the process of developing and perfecting their range of operating loans to meet the cash flow needs of these businesses. This will require the use of rating systems that enable lenders to assess different types of risk and act quickly to meet customers financial needs.

El Karm also pointed to the need to modernise the legal framework for commercial paper, as the current legislation does not sufficiently protect creditors, particularly in terms of cumbersome and complex procedures involved.

He noted that (the rejection rate for cheques at the clearing house is no more than 2%, compared with around 12% for presented bills of exchange).

For individuals, he called for the development of banking services in the area of consumer credit. To help banks and other creditors to increase consumer credit, he suggested speeding up the creation of credit information companies, known as "credit bureaus", whose legal framework will be adopted in 2022, pointing out that one such company has been authorised by the Central Bank of Tunisia (BCT) but has not yet been able to start operating.

Asked about the financial impact of business and consumer credit on companies and individuals, El Karm believes that the widespread use of this type of credit and the improved management of the risk associated with it will make it possible to reach a much larger population and create a mass dynamic that will make it possible to negotiate the conditions under which these loans are granted, with a view to possibly easing them.

The banking expert believes that banks and factoring companies can play an important role in the success of this transition to less orthodox credit instruments by providing the market with viable, modern alternatives to backdated cheques.

He added: I believe that Tunisian banks are now well equipped and have the necessary expertise to provide the necessary alternatives. The state must also play its part by making the appropriate regulatory adjustments, providing sympathetic support for this process and removing any obstacles to improving the credibility of these new instruments.

(The cheque law is part of a series of breakthrough reforms, which often require adjustments that can be costly to implement in the short term. Breakthrough reforms also require fine-tuned, intelligent management of the phase-in period. But breakthrough reforms are still an opportunity to be seized in order to modernise the national payment system, to free the Tunisian economy from the predominance of banknotes and cheques, to give more concrete meaning to the national policy of decashing, and to bring a large number of operators out of the informal market,) he said.

He concluded by saying that (during the transition period, we must focus on being close to citizens and businesses in order to manage any bottlenecks that may arise and to ensure the success of the desired transition to a more modern and digitalised economy, particularly in terms of payment and financial instruments).

English: Samir Ben Romdhane

Posted in:

News

Related posts

-

Smau Milan 2022

Participation of our startup in the SMAU Milan 2022 fairRead more

Smau Milan 2022

Participation of our startup in the SMAU Milan 2022 fairRead more -

Solution de location de camions avec chauffeur adaptées à un budget transport maîtrisé

Solution de location de camions avec chauffeur adaptées à un budget transport maîtriséRead more

Solution de location de camions avec chauffeur adaptées à un budget transport maîtrisé

Solution de location de camions avec chauffeur adaptées à un budget transport maîtriséRead more -

Solutions d’optimisation des coûts de logistique sur mesures pour un budget de transport maîtrisé

Solutions d’optimisation des coûts de logistique sur mesures pour un budget de transport maîtriséRead more

Solutions d’optimisation des coûts de logistique sur mesures pour un budget de transport maîtrisé

Solutions d’optimisation des coûts de logistique sur mesures pour un budget de transport maîtriséRead more -

O'Express the home delivery service

O'Express the home delivery serviceRead more

O'Express the home delivery service

O'Express the home delivery serviceRead more -

Exports to Sub-Saharan Africa: The State covers 50% of insurance premiums

Exports to Sub-Saharan Africa: The State covers 50% of insurance premiumsRead more

Exports to Sub-Saharan Africa: The State covers 50% of insurance premiums

Exports to Sub-Saharan Africa: The State covers 50% of insurance premiumsRead more

Leave a comment